Most insurance due diligence focuses on claims-made policies and determining whether these need to be tailed out. The reason is that these policies tend to include change-in-control provisions that cause them to terminate or enter run-off, failing to cover pre-close wrongful acts that materialize into claims after closing.

These policies typically include Directors & Officers Liability, Employment Practices Liability, Fiduciary Liability, Errors & Omissions Liability and Cyber Liability.

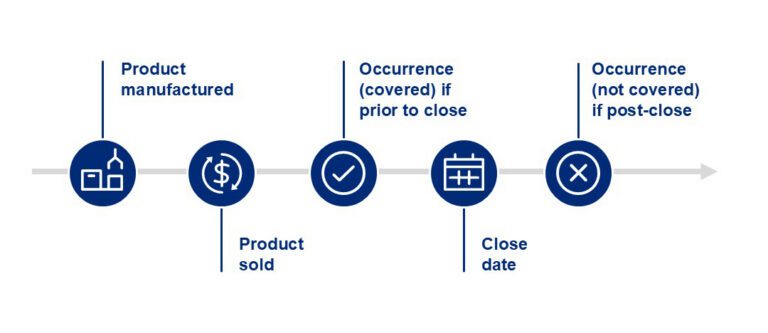

However, there is an occurrence policy that is equally important and can have dire consequences if not addressed correctly: the general liability policy.

General liability policies cover bodily injury and property damage caused by products and complete operations. Since they are occurrence policies, the incident (or “occurrence”) must take place during the policy period. The claim can still be covered even after the policy is terminated.

But what if an occurrence doesn’t take place until after closing and termination of the policy? Unfortunately, buyers rarely ask this question. It can make the difference between realizing an ROI on an investment or not.

For example, let’s say you’re acquiring a manufacturer of vehicle brake calipers. You have 400,000 units across 100,000 vehicles in the U.S. There is no clear indication of any fault with the brake pads, no customer complaints, recalls, etc. However, six months after acquiring the company, a flaw in the caliper led them to get stuck in freezing temperatures, leading to brake failure and an increase in accidents, even fatalities.

Is the occurrence of the manufacturing of the caliper, installation of the caliper or the failure of the product?

Which policy would cover the loss? The seller’s pre-close policy? The buyer’s go-forward policy?

Proper coordination of these policies can make all the difference.

In this situation, the occurrence may be determined to have been the failure of the calipers. Let’s assume this is also an asset sale, with the policy terminating upon close. It could also have been an equity transaction, where the buyer would have assumed any liability under their general liability policy.

Regardless, there are two options the buyer should look into.

First, the buyer can discuss with their insurance carrier in advance whether liability for any products they acquire is automatically covered by their policy. General liability policies can include provisions providing coverage for newly acquired products. However, this is not always the case. Buyers should also confirm whether that includes products already purchased by customers or only those included as inventory. This is the easier and less expensive option.

Second, buyers can work with sellers to arrange for a discontinued product tail. This would essentially extend coverage to claims arising from products the seller has already manufactured and sold to customers. While this would be more costly, it would isolate losses for these products to the tail policy, preventing impact on the buyer’s general liability policy.

As always, buyers should be presented with all options and determine what is in their best interest based on their risk tolerance.

Mike Richmond

Mike is a Senior Vice President at The Horton Group. As a trusted business advisor, he is responsible for analyzing every detail of a client’s business, determining every exposure and providing risk management programs to insulate his clients’ businesses from liability. Mik is also an attorney who studied law at night while working as an insurance consultant. His legal education gives him an intimate understanding of the liabilities businesses face, as well as the many ways those liabilities can affect businesses.

Material posted on this website is for informational purposes only and does not constitute a legal opinion or medical advice. Contact your legal representative or medical professional for information specific to your legal or medical needs.